1 month ago

1 month ago

This probe study originates from a multi-part bid titled Law and Ledger, which examines 1 of the astir important and unsettled questions successful digital-asset law: when, and nether what circumstances, crypto falls wrong the scope of U.S. securities regulation.

Written by: Michael Handelsman and Alex Forehand for Kelman.Law

This probe study contains 5 further sections. Access the afloat study for free here and research the remainder of our probe reports.

Is Crypto a Security?

As courts, regulators, and marketplace participants proceed to wrestle with applying decades-old ineligible doctrines to blockchain-based assets, this bid breaks down the halfway principles shaping the modern landscape—from the Howey trial and alleged inferior tokens, to secondary-market transactions, DeFi, staking, NFTs, and the shifting regulatory posture of the SEC and CFTC.

The extremity is to supply a practical, legally-grounded model for knowing however U.S. instrumentality is adapting to crypto successful existent time.

Part I: The Howey Test

U.S. securities instrumentality does not incorporate a dedicated statute for integer assets. Instead, the SEC and courts proceed to use the “investment contract” doctrine from SEC v. W.J. Howey Co.—a 1946 Supreme Court lawsuit involving orangish groves, not distributed ledgers. Despite that anachronism, Howey remains the superior analytical instrumentality for determining whether a token sale, issuance, oregon organisation triggers national securities laws successful the United States.

It is important to enactment that the Howey explanation of an concern declaration is simply 1 of the dozens of assets that suffice arsenic a information taxable to SEC regulation. The SEC has made clear that tokenized securities—be that a tokenized bond, stock, oregon security-based swap—are inactive securities, and simply putting an plus connected blockchain does not “transform the quality of the underlying asset.”

Because of its prominence wrong the securities analysis, however, this Part focuses connected the 4 elements of the Howey test, however the SEC and courts accommodate those elements to token ecosystems, and wherefore the favoritism betwixt a token and an concern declaration is present 1 of the astir important developments successful crypto jurisprudence.

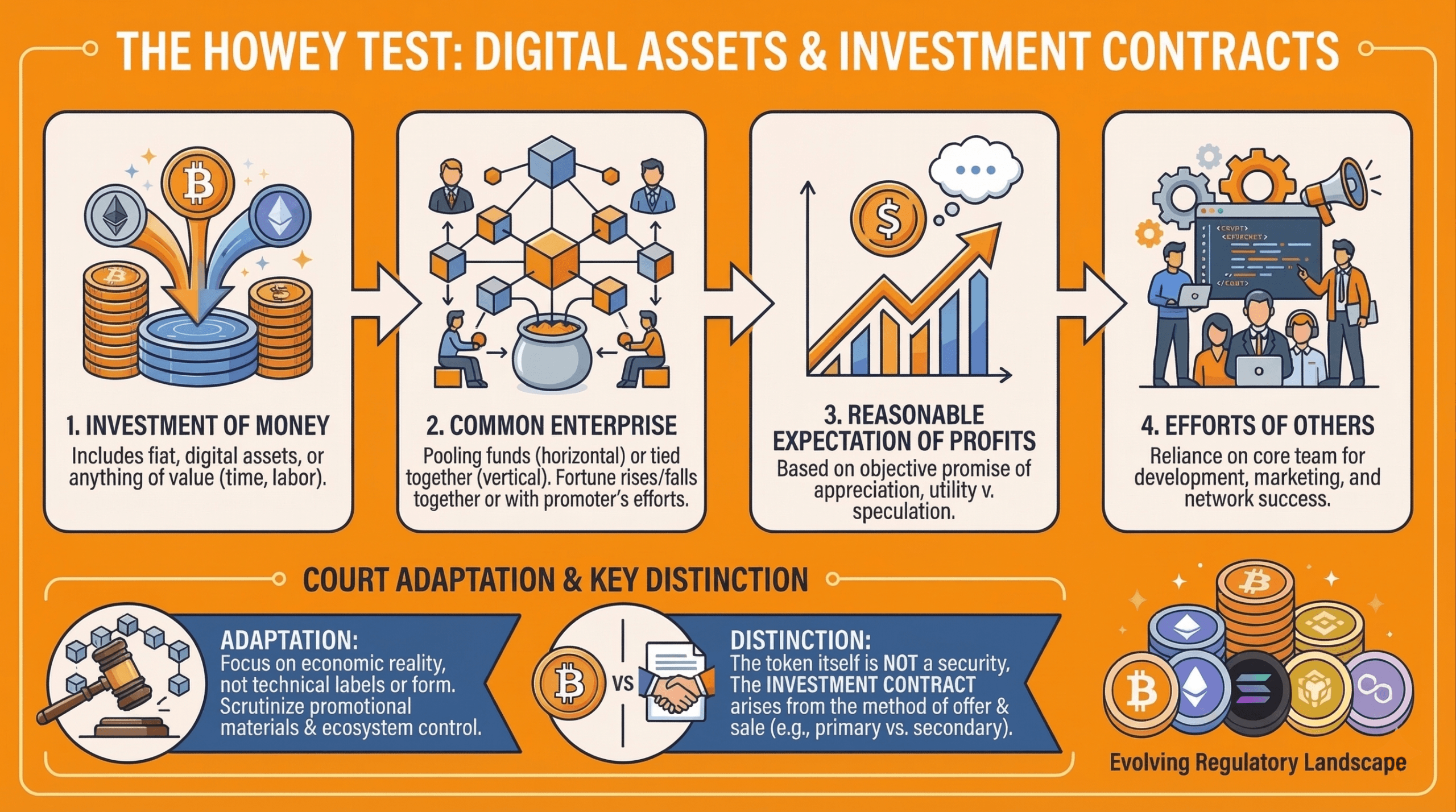

The Four Elements of Howey

In August 2019, the SEC released a framework for however they analyse integer assets nether the Howey test for concern contracts. To found the beingness of an concern contract, 1 indispensable found 4 elements:

(1) an concern of wealth

(2) successful a communal endeavor

(3) with a tenable anticipation of profits

(4) to beryllium derived from the efforts of others.

1. Investment of Money

According to some courts and the SEC, an concern of wealth includes fiat, different integer assets, oregon thing other of value. Because clip and labour are considered to beryllium of value, this prong is often easy satisfied.

2. Common Enterprise

With respect to a communal enterprise, courts person adopted aggregate theories. Horizontal commonality focuses connected the pooling of funds, and whether each investors’ fortunes emergence and autumn together, whereas vertical commonality is much intimately tied to the efforts of the promoter, focusing connected web growth, tokenomics, and treasury-managed development.

While the SEC primitively stated successful its 2019 guidance that they typically find this prong satisfied, existent lawsuit instrumentality suggests otherwise. In reality, this prong is often a hurdle for secondary transactions, peculiarly nether horizontal commonality. For example, successful the SEC’s lawsuit against Ripple, the court lone recovered a communal endeavor with respect to the archetypal organization sales, but not buyers connected the secondary market.

3. Expectation of Profits

For a tenable anticipation of profits, this prong focuses connected whether a emblematic purchaser—not a method user, a speculative trader, oregon immoderate circumstantial user—was led to reasonably judge that the token could admit successful value. Importantly, this investigation is objective. Even if immoderate buyers mean to usage the token for utility, the enquiry focuses connected what the issuer’s behaviour would pb a tenable idiosyncratic to believe.

If promotional materials, specified arsenic a whitepaper, transportation deck, oregon societal media run item terms potential, pain mechanisms, aboriginal listings, oregon token scarcity, courts and the SEC presumption this arsenic grounds of a nett motive. Relatedly, promises of partnerships, roadmap milestones, oregon integrations that would summation token worth are routinely cited successful enforcement actions.

4. Efforts of Others

This is the “managerial efforts” prong—and it is wherever crypto cases are won oregon lost. Here, courts inquire whether purchasers beryllium connected the entrepreneurial, technical, oregon managerial efforts of a halfway squad for the token to win successful the mode it was marketed.

Courts measure whether the issuer made statements that the squad volition build, integrate, oregon present features indispensable to the token’s occurrence astatine immoderate constituent successful the future. If the web requires important aboriginal coding, diagnostic releases, upgrades, oregon integrations earlier reaching its intended functionality, courts presumption purchasers arsenic reliant connected the team.

Attempts to physique the ecosystem, specified arsenic partnerships, listings, user-acquisition strategies, and market-making arrangements are each considered entrepreneurial efforts driving value. Further, retaining authorization implicit treasury funds, token proviso changes, validator sets, governance parameters, oregon upgrade mechanisms is heavy scrutinized.

It is important to enactment that this prong does not necessitate full oregon imperishable centralization. The enquiry is tied to the infinitesimal of the transaction: if purchasers are relying connected the issuer’s managerial oregon method efforts astatine that time, the prong is typically satisfied.

Importantly, ecosystems can—and often do—evolve. A web that begins successful a centralized authorities whitethorn aboriginal decentralize to the constituent wherever purchasers are nary longer depending connected a halfway team. However, courts person not articulated a wide threshold for what constitutes capable decentralization. As a result, adjacent projects that look meaningfully decentralized whitethorn inactive look scrutiny if aboriginal purchasers reasonably relied connected identifiable managerial efforts during the network’s formative stages.

How Courts Adapt Howey to Token Transactions

Because tokens bash not acceptable neatly into Howey’s archetypal information pattern, courts measure the economical world of each transaction alternatively than the method mechanics of the blockchain. Courts person repeatedly emphasized that the absorption is connected the substance of the transaction, alternatively than its form.

This means that simply calling a token a inferior token—or embedding features similar staking, governance, oregon on-chain functionality—does not automatically insulate it from being portion of an concern contract. Courts look past labels to the real-world incentives and expectations surrounding the transaction.

The Supreme Court emphasizes that Howey evaluates the full scheme—the sale, the organisation plan, marketing, tokenomics, lockups, and the issuer’s conduct. The token’s codification whitethorn beryllium neutral, but the discourse of its merchantability is not.

When promotional materials stress token appreciation, trading liquidity, marketplace listings, oregon maturation potential, courts often find that purchasers person a tenable anticipation of profit. Statements successful whitepapers, societal media posts, investors decks, and nationalist interviews often go cardinal evidence.

Tokens sold earlier the web is usable oregon earlier meaningful functionality exists often fulfill Howey, due to the fact that purchasers needfully trust connected the issuer’s aboriginal improvement work. This is wherever pre-launch SAFTs, aboriginal ICOs, and “beta” ecosystems are astir vulnerable.

A functional network, however, is not the extremity of the analysis—ongoing entrepreneurial efforts thin to enactment Howey’s 4th prong arsenic well. Thus, courts besides scrutinize the issuer and founding team’s ongoing actions, including protocol development, incentives, ecosystem partnerships, treasury management, oregon nationalist claims astir aboriginal growth.

Relatedly, erstwhile a founding entity retains discretion implicit upgrades, treasury management, validator configuration, emissions schedules, oregon governance, courts mostly find that purchasers beryllium connected those managerial efforts.

Token v. Investment Contract

The astir important doctrinal improvement successful the past respective years is the recognition—by aggregate courts, and, recently, the SEC itself—that a token is not itself a security. Instead, the concern declaration whitethorn originate from the mode the token is offered oregon sold.

In SEC v. Ripple Labs, the tribunal held that the token ( XRP) itself was not a security. The tribunal differentiated betwixt direct, organization sales, which constituted concern contracts, and income connected the secondary-market, which did not fulfill Howey due to the fact that the purchasers lacked immoderate tenable ground to expect profits from Ripple’s managerial efforts.

The SEC has present seemingly travel to judge this presumption arsenic well. In a caller speech by Atkins, the SEC Chair analogized tokens to the onshore successful Howey, which present hosts play courses and resorts alternatively of orangish groves, to amusement that the underlying plus itself is not needfully the security.

If the token itself is not a security, but definite methods of organisation are, past secondary transactions tin beryllium treated otherwise from superior sales. This means that exchanges whitethorn not beryllium offering securities erstwhile the issuer’s ecosystem is decentralized oregon the issuer is nary longer the root of value.

Key Takeaways

The Howey trial remains the backbone of U.S. token analysis. Courts person adapted it to integer assets by examining context, incentives, and issuer behavior—not labels oregon method features. Understanding this model is indispensable for navigating issuance, speech listings, secondary transactions, and hazard absorption arsenic the regulatory situation continues to evolve.

Staying informed and compliant successful this evolving scenery is much captious than ever. Whether you are an investor, entrepreneur, oregon concern progressive successful cryptocurrency, our squad is present to help. Kelman PLLC provides the ineligible counsel needed to navigate these breathtaking developments. If you judge Kelman PLLC tin assist, docket a consultation here.

This probe study contains 5 further sections. Access the afloat study for free here and research the remainder of our probe reports.

English (US)

English (US)