1 year ago

1 year ago

Monday’s trading league volition spell down arsenic 1 of the astir volatile since the COVID clang successful March 2020, with planetary markets caught successful the crossfire arsenic the U.S. and China look disconnected implicit tariffs and neither superpower shows immoderate impulse to backmost down.

As equity markets teetered, the volatility spilled into each plus class. Bitcoin (BTC), for example, swung arsenic overmuch arsenic 10% intraday. The existent focus, however, is connected the U.S. 10-year Treasury yield. That's the alleged risk-free involvement rate, which the Trump medication said it wants to little arsenic it looks to refinance trillions successful nationalist debt.

The output dropped to 3.9% from 4.8% precocious past week aft President Donald Trump bolstered commercialized tensions with sweeping import tariffs, boosting request for the Treasury notes.

Bond prices typically rise, sending yields lower, erstwhile Wall Street turns hazard averse. Unusually, arsenic the risk-aversion accrued connected Monday, yields turned higher, jumping to 4.22%.

This spike wasn’t confined to the U.S. The U.K. experienced its sharpest complaint leap since the Liz Truss-era pension crisis successful October 2022, and yields roseate globally, signaling increasing instability and diminishing assurance successful sovereign indebtedness and currencies.

Ole S Hansen, the caput of commodity strategy astatine Saxobank, pointed to the standard of the determination successful long-dated Treasuries arsenic a motion of thing deeper perchance unfolding.

“U.S. Treasuries suffered a monolithic sell-off yesterday, with agelong yields rising the astir since the turbulence during the pandemic outbreak—a imaginable motion of ample holders of Treasuries, specified arsenic overseas holders, selling and repatriating their assets," Hansen said successful a station connected X. "The 30-year U.S. Treasury benchmark roseate from lows adjacent 4.30% to arsenic precocious arsenic 4.65% yesterday, portion the 10-year benchmark lifted backmost to 4.17% from a debased adjacent 3.85% the anterior day.”

While Hansen pointed fingers astatine overseas selling, particularly China, which is said to person offloaded $50 cardinal successful Treasuries, Jim Bianco, president of Bianco Research, challenged that narrative.

“No, foreigners were not selling Treasuries to punish the U.S. (Trump),” helium wrote, pointing alternatively to a crisp rally successful the Dollar Index (DXY), which climbed 2.2% successful conscionable 3 days.

“If China oregon different foreigners were selling Treasuries ... they would person to person those dollars to a overseas currency. Otherwise, selling Treasuries and leaving the wealth successful dollars successful a U.S. slope is pointless. If they sold capable Treasuries to plaything yields ... the consequent selling of dollars ... would person driven down the dollar. Instead, it rallied much than usual.

“This suggests that overseas wealth was moving into the U.S., not distant from it ... the selling was much home and much acrophobic astir inflation.”

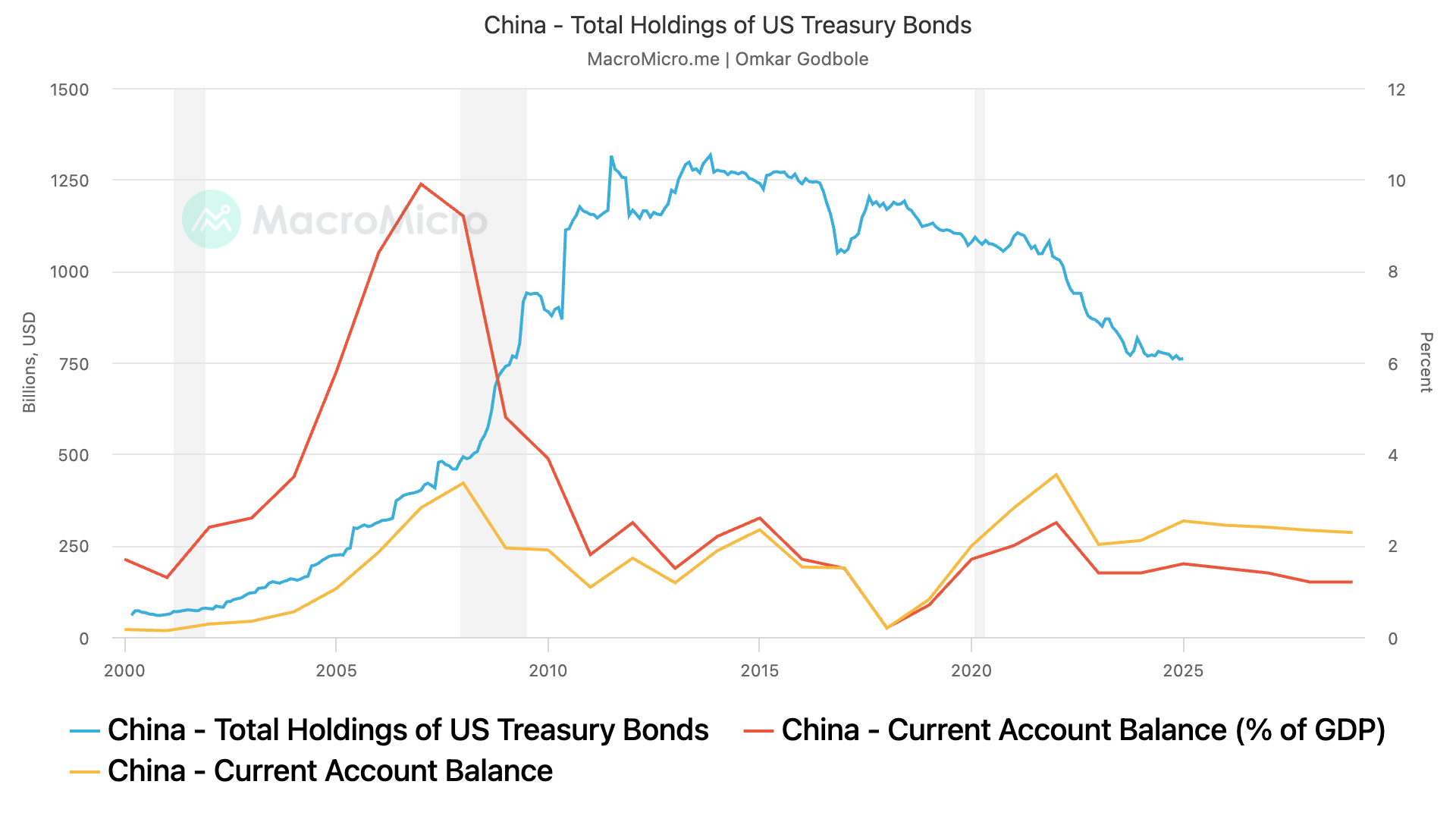

Despite these views, unconfirmed reports astir China's income proceed to circulate. As of January 2025, China inactive held approximately $761 billion successful U.S. authorities debt, the largest proprietor aft Japan.

The communicative that the 10-year and 30-year yields surged connected Chinese is unconvincing due to the fact that astir of the authoritative Chinese investments successful dollar-denominated assets are not successful longer duration instruments, but bureau bonds, shorter-term bills and slope deposits.

There is simply a cognition China tin summation leverage successful the commercialized warfare done its holdings of U.S. Treasury notes. That's not needfully true.

As the economist and writer of "The Great Rebalancing: Trade, Conflict, and the Perilous Road Ahead for the World Economy" Michael Pettis has agelong argued, China's holdings of U.S. Treasury bonds are straight linked to its existent relationship surplus and it cannot weaponize these holdings against the U.S.

It's nary astonishment that China has been lightening up its Treasury investments since 2013 with its existent relationship surplus peaking during the 2008 crash.

English (US)

English (US)